Monese gives consumers peace of mind with embedded insurance

2M+

$201M

31

In a nutshell

New accounts, new embedded insurance

As fintechs mature, they need to integrate new strategies to remain competitive. That can be especially challenging during the pandemic, when customers’ sources of income can be wildly unpredictable.

And for Monese, that’s where embedded insurance comes in. The mobile banking app’s services largely cater to those with nontraditional work and income patterns, many of whom are concerned about their future employment or ability to work.

‘The pandemic has drastically changed our behaviour, especially when it comes to finances,’ says Monese CEO Norris Koppel. ‘Consumers are doing more online, creating a greater demand for instant goods and services. What’s more, [the pandemic] has forced many people to think about their own financial security – making the protection offered by products like insurance very valuable to consumers.’

As Monese set out to revamp their paid accounts in the UK, they decided that protecting their customers and giving them peace of mind was a top priority. So they asked their customers which features they needed the most from their account. Bills and purchase protection were among the top responses – so Monese knew that their customers were looking for added security.

Listen to Sarah Holt, Head of Partnerships at Monese, talk about their embedded insurance program:

‘The pandemic has drastically changed our behaviour, especially when it comes to finances. Consumers are doing more online, creating a greater demand for instant goods and services. What’s more, [the pandemic] has forced many people to think about their own financial security – making the protection offered by products like insurance very valuable to consumers.’

‘This insurance is so simple and easy. That was essential for us – it had to be seamless and managed in-app.’

Qover creates new insurance product to protect Monese customers amidst pandemic

In order to create a post-pandemic safety net for their account holders, Monese looked for a partner that shared the same digital, Pan-European values.

At Qover, we know that there’s no one-size-fits-all when it comes to embedded insurance, which is why we opt for a collaborative process with our partners. We worked together with Monese to make sure that the solution was 100% adapted to the needs of its users.

‘From the outset, Qover understood what we were trying to achieve and worked very collaboratively with our team in order to deliver a product that worked for our customers,’ Koppel says. ‘We put together a cross-functional team on both sides, so when complexities and challenges arose, we were able to face them head on and tackle them together. It was a real team effort.’

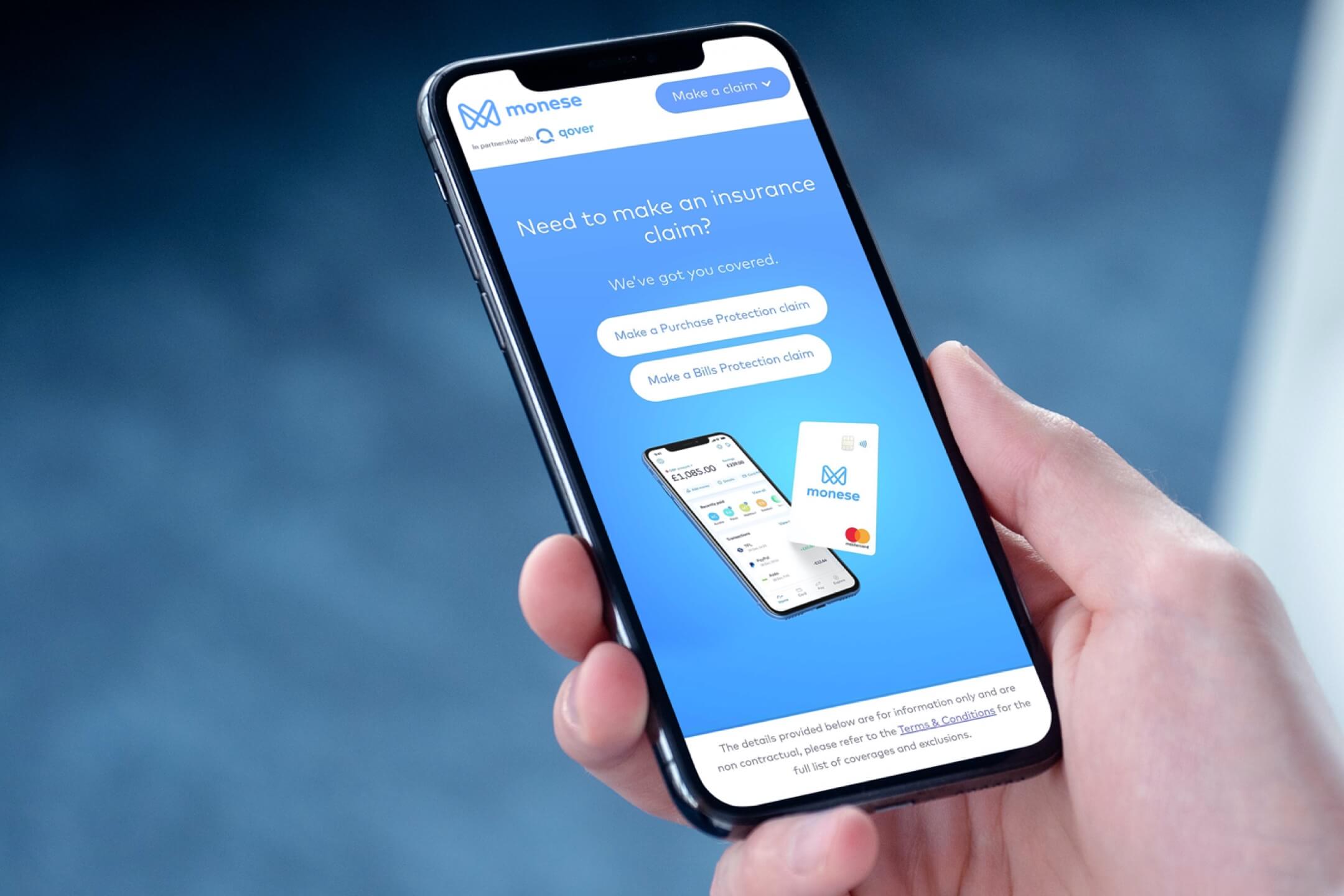

To that end, we created a brand new product – bills protection – which is automatically included in all of Monese’s paid plans (Essential, Classic, Premium). This solution covers monthly regular bills in case of accident, sickness or involuntary unemployment – the first of its kind on the UK market as a response to COVID.

Seamless insurance with a fully digital customer experience

The Classic and Premium plans also come with purchase protection, which offers theft and damage insurance on debit card purchases, including electronic devices like mobile phones.

Not only are these insurance products easily integrated into Monese’s mobile app – and paid cards – but we took the user experience one step further by allowing customers to file a claim or even submit an invoice (in the case of bills protection) online.

‘This insurance is so simple and easy,’ Koppel says. ‘That was essential for us – it had to be seamless and managed in-app.’

What’s more, Qover’s pan-European heritage is uniquely positioned to help Monese expand to other countries in the future.

‘Our values are very closely aligned,’ Koppel says. ‘We both serve a pan-European consumer and we’re both focused on providing accessible services. Qover really understands our audience and the value of creating a product that can empower those who are often overlooked by traditional financial services.’

‘Our values are very closely aligned. We both serve a pan-European consumer and we’re both focused on providing accessible services. Qover really understands our audience and the value of creating a product that can empower those who are often overlooked by traditional financial services.’